In India, a private trust covers the structure of creating a secure future for a special needs dependent. Through a private trust, the parents can choose to manage the child’s affairs as they wish to. It also ensures that the legacy left for the special needs child is managed to provide for the child’s lifetime care needs. Though a trustee manages the affairs, they never own the trust assets, which brings a fiduciary nature when a trust is functioning. This helps in addressing the concerns of the parents when they are no more.

Who Can Set Up A Special Needs Trust?

There is no restriction in the Indian Trust Act as to who can set up a family private trust. Parents, Siblings, grandparents, or a Legal guardian can set up a trust for the special needs child’s future. Settlor doesn’t need to be a trustee of the trust. If separate people are identified, then the settlor can only create a trust, while trustees will manage the trust. Alternatively, the initial trustee/s can also be the settlor. The benefit they derive from this is that they can manage the affairs well, knowing their special needs child. The future trustees, if identified, can join as co-trustees and can fill their place when they are not around.

Four-Step Process

Step 1

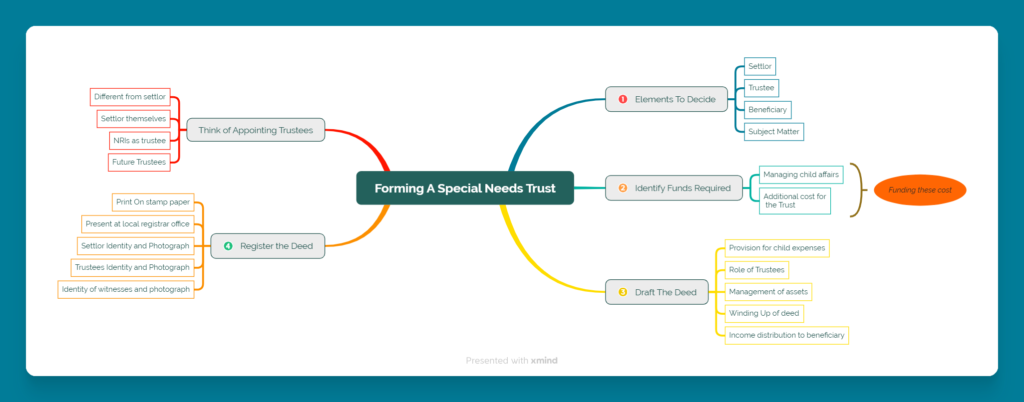

Identify the Elements Required

A private trust has four elements:

– Settlor, Beneficiary, Trustee, and the subject matter. Since you are the settlor so the first element is taken care of. You need to identify who will be the trustees. The settlor can be the initial trustees, but it’s good to identify who will be the future trustees. If you have it from your family, then it surely eases your stress. But if not, then you can even have professional trustees. Then you need to identify the beneficiary, which in this case will be the special needs child. But if you are looking to add another as a beneficiary, you can do so. The last is the subject matter of trust, i.e, assets. Which assets trust will hold, and at what time, is important. You will have to analyze how these assets will pass on trust so that you can plan accordingly. All these elements are important to address and start creating trust.

Step 2

Estimate the Funds Required

One of the major considerations while setting up a trust is to identify the funds the trust will require. These funds should be enough to manage child affairs and bear the cost of trust if any. Having said that, identifying the lifetime care cost of a special needs dependent is important. Without which, it will be difficult to know how much funding should be left for the trust. Identifying the lifetime cost of care is a complete financial planning exercise for which various factors need to be considered. Life expectancy, inflation, returns, etc. Then there is a cost which a trust may incur additionally, such as accounts management, managing investments, and professional fees. Etc. These costs will be incurred from the corpus left for the child, which means the requirement will be a bit higher than just the child’s expenses. Who will fund this cost, and where can the funds be arranged, needs to be decided first.

Step 3

Preparing a trust deed

Once the funds are known, then the formation of a trust deed is important. A trust deed is the legal document that validates the setting up of a private trust. The drafting of the trust deed is the most crucial element because this will be the basis on which the trust will function. The trust deed ideally should carry all the provisions- The rule and power of trustees, management of funds, dos and don’ts, income distribution to the beneficiary, and the winding up of the trust all need to be written in the trust deed. It’s advisable that an expert’s help is sought, considering the legality and complexities involved in the functioning of a trust.

Step 4

Registering a Trust

Registration of a trust in India is not mandatory. However, in situations where trust is not created by will and involves an immovable property, then it needs to be registered. Even if immovable property is not involved, it is recommended to register the trust. The process of registration of the trust deed is as follows:

- The trust deed is first to be printed on a stamp paper of the requisite value

- The deed is to be presented at the local register under the Indian Trust Act of 1882

- One passport-size photograph & a copy of the proof of identity of the settler

- One passport-size photograph & a copy of the proof of identity of each of the two trustees.

- One passport-size photograph & a copy of the proof of identity of each of the two witnesses.

- Signature of settlor on all the pages of the Trust Deed

- Witnessed by two people on the Trust Deed.

- Go to the local registrar & submit the Trust Deed, along with one Photocopy, for registration. The photocopy of the Deed should also contain the signature of the settlor on all the pages. At the time of registration, the settler & two witnesses are required to be personally present, along with their identity proof in the original.

- The Registrar retains the photocopy & returns the original registered copy of the Trust Deed.

Appointing Trustees

If trustees are different from the settlor, then they can be appointed right at the formation of the trust. But if the settlor will work as a trustee, and if future trustees are identified, the trust can ask them to be appointed later. After registration, it’s the trustee who appoints the future trustees. Any individual, corporate, or professional can be appointed as a trustee. The cost of the trustee will be borne by the trust. But finding the right institution may be difficult since most families do not have access to their services. That’s where we come in.

One of the important considerations for all families is from NRIs. Such families with special needs children wish to settle in India because they have the social environment here. They can form trust for their children in India before their resident status is converted to NRIs. However, there are restrictions for becoming the initial trustees with NRI resident Indian Status. Section 73 and Section 75 of the Indian Trust Act, 1882 mandate replacing the trustee if the current trustee stays outside India for more than six months. These rules specifications don’t allow NRIs to become the initial trustee of the Indian Trust.